My startup YesGraph just went through the Y Combinator Winter 2015 batch. (YesGraph helps your app grow. Check it out). I get asked all the time by folks that haven’t been through YC whether it was worth it. Many people that don’t understand fundraising and dilution enough to even calculate this. So let’s walk through the numbers.

Most people think: ok, they take 7%, so you need to be 7% more valuable to justify the investment. Maybe if you understand fractions, you know you need to be 1/(1-7%) = 7.5% more valuable to make it up. This is completely wrong math.

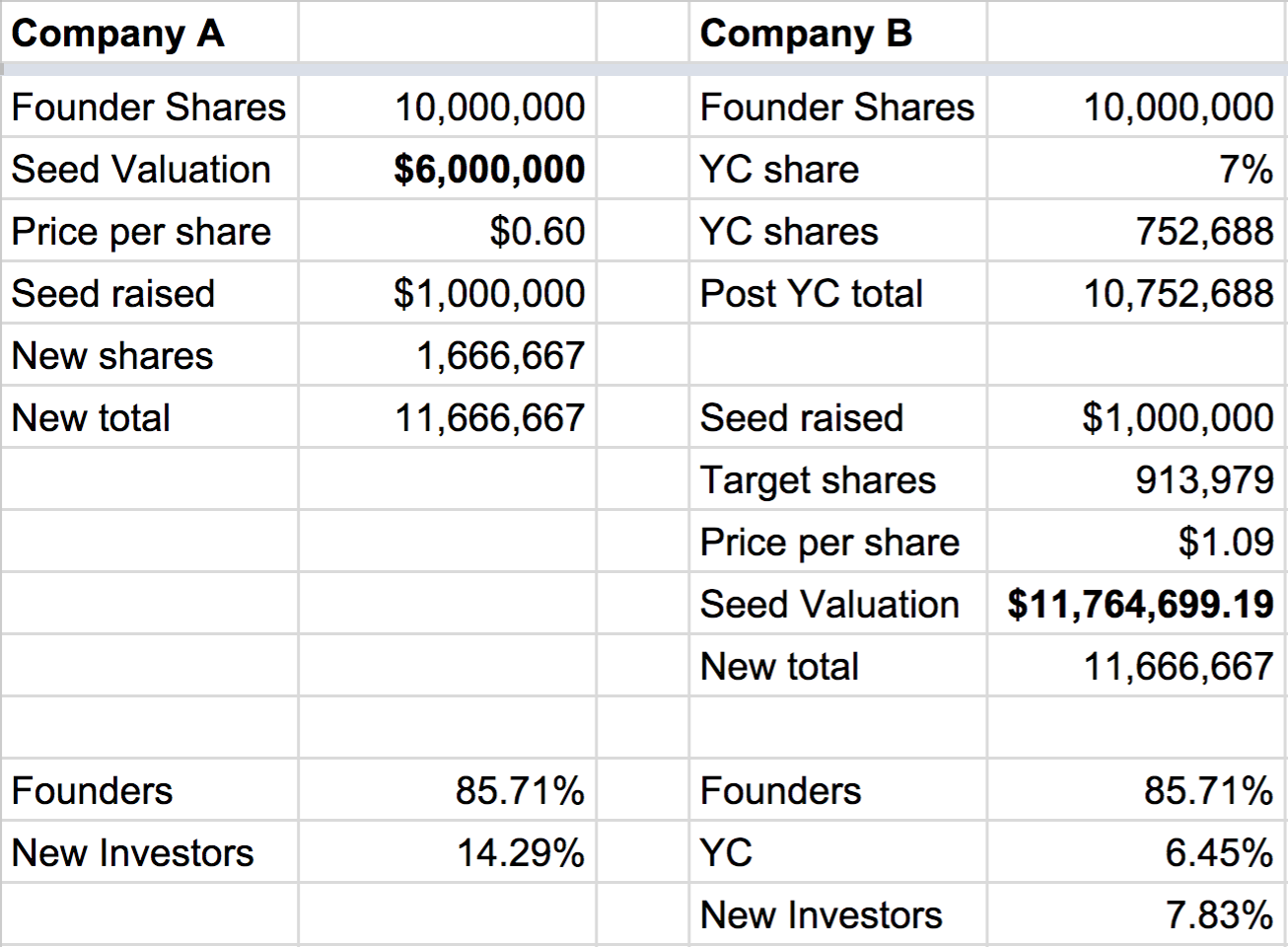

To match the dilution from their investment, you need to have a far higher valuation of your next round. Let’s walk through an example.

Company A doesn’t go through YC, but eventually raises $1M on a pre-money valuation of $6M. They will end up giving up $1M / ($1M + $6M) in dilution, or 14.2%.

Company B does go through YC. So that means 7% dilution. Then let’s say that the company raises that $1M seed. What does the valuation need to be to hit 14.2% dilution total?

7.5% higher would mean around $6.5M.

Actually it needs to be $11.7M pre to reach the same dilution. That is a 96% higher.

Here is a table to illustrate why, and here is a link to the source spreadsheet. In short, to target the same total dilution, you need to give up less in the seed round.

But this math is also wrong!

This assumes only one round. If YC makes your startup more valuable for your Seed plus Series A and Series B, then you can amortize the dilution across multiple rounds.

This gives a hint about why all this math is wrong. Sure, you have multiple rounds, but what is your real goal? You want your startup to win. You want it to be a breakaway success that makes a lasting impact in the world.

If you do, you are rewarded handsomely. This is why VCs have power law returns. The breakaway successes are worth 100X those that fail.

So how do we calculate value on a long enough time horizon, like 5 or 10 years? It turns out it is binary: did you win or not?

That valuation? That is really based only on the likelihood of winning. A $6M or $12M valuation is really just saying there is a 0.6% or 1.2% chance of being worth $1 Billion.

That changes the calculus. You might ask, are we 7% more likely to win? This is only a single shot, and not some statistical exercise with expected values over thousands of trials. So you could also round the question to: are we more likely to win?

I think the answer is unambiguously yes. This is a great rubric for thinking about your company generally. Are we more likely to win with this hire? Will this new product push make us win? Will this new investor help us win?

To be clear, the wrong choices for those questions can easily be a resounding, “No!”

There are negative hires. There are investors that suck. You make wrong product decisions all the time.

But the YC advice, the cred that it gives you, and, yes, the boost in your fundraising efforts, all make it a YES.

This was actually my second time through YC. I also went through in W08, and a lot has changed since then. If you want to get the next post about what changed since, subscribe here. And if you want your company to grow faster, go signup for YesGraph.